Level offers organizations a product for on-demand pay, allowing employees to access their earnings as they work, instead of waiting for the end of the pay period. This empowers employees with financial control, reducing the need for high-interest loans. Providing on-demand pay helps companies differentiate themselves in the job market, with 57% of workers preferring it over extra paid holidays.

Product goal: Provide services to as many companies as possible by providing benefits for both employers and employees.

“Tools like Level will, we believe, become utility services that every employer offers, just like a gym membership or pension.“

— Level CEO

My goal: Create a savings flow for users as a part of a broader strategy of improving peoples’ financial well-being.

Without having access to the users we turned to behavioral science and crafted a saving flow for the on-demand payment app. The integration of the flow marked the last milestone before the product's official release. With its inclusion in the app, users gained access to a seamless tool for financial planning and the company was able to gain partners.

Our mission was to revolutionize the way individuals manage their finances, combating the detrimental effects of the poverty premium while catering to the needs of both employers and employees.

But the solution is aimed at other companies, B2B in other words. What is the value for business you might ask?

Value For Employees:

No need for short-term loans. Workers can save directly from their pay before it reaches their bank account, nudging them to save more and often for the first time.

Covering unexpected expenses. Pay on-demand allows people to meet these surprise costs without waiting for their next paycheck.

Value For Companies:

Attracting workers by providing on-demand pay as a benefit

Decrease employee turnover

Workers are more willing to take additional shifts when they see an instant payoff

Switch to monthly pay (Monthly pay for the company, any-day pay for staff).

When I joined the team, the feature for on-demand payments was already developed. This allowed client companies to offer their employees the ability to access their payments daily, as opposed to the traditional monthly or bi-monthly payments.

61%

of employed UK adults stated that money worries were their biggest cause of stress

27%

feel financial stress on a daily basis

50%

don’t have enough saved up to pay an unexpected bill

80%

aren’t saving enough

By holding all income streams in one place, our app eliminates the need for users to transfer money elsewhere. This simplicity encourages saving, as easy actions are more likely to be adopted. With reduced financial worries, employees can unlock their full potential at work.

We didn't have direct access to our potential users, but luckily the topic was extensively researched, allowing us to make informed assumptions. Our aim was not only to enable conscious users to begin saving but also to nudge others to do the same. According to the Fogg Behavior Model, three elements must align for a behavior to occur: Motivation, Ability, and Prompt.

The best way to start is to identify moments when someone’s motivation to change is very high and then offer them what he calls ‘hot triggers’ which give them the opportunity to enact a new behavior. We pinpointed payday as a crucial moment when individuals are highly motivated to make changes. Taking advantage of this, we crafted a savings mechanism seamlessly integrated into the payroll process. This enables users to allocate a portion of their earnings directly to savings prior to receiving their paycheck.

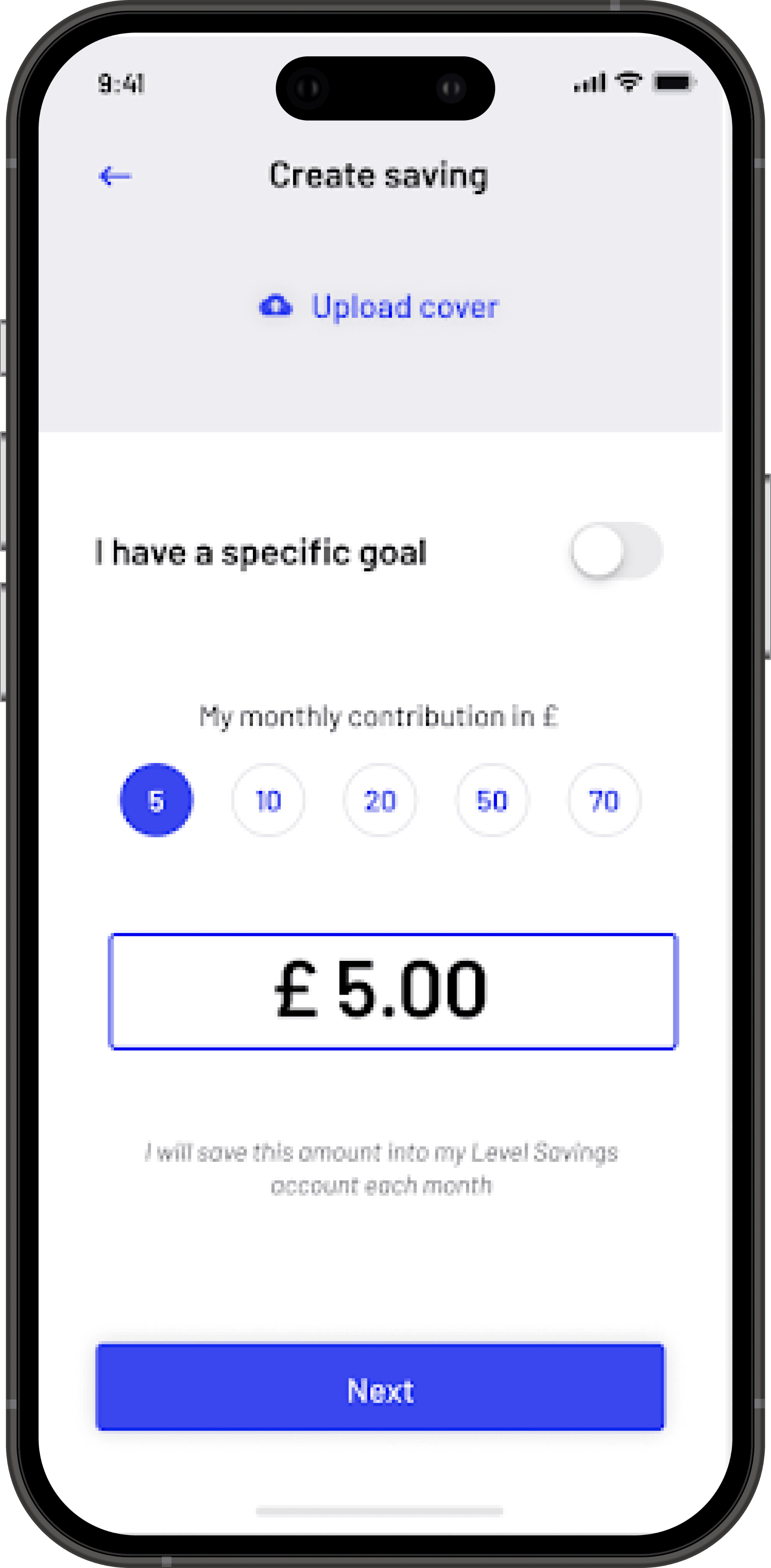

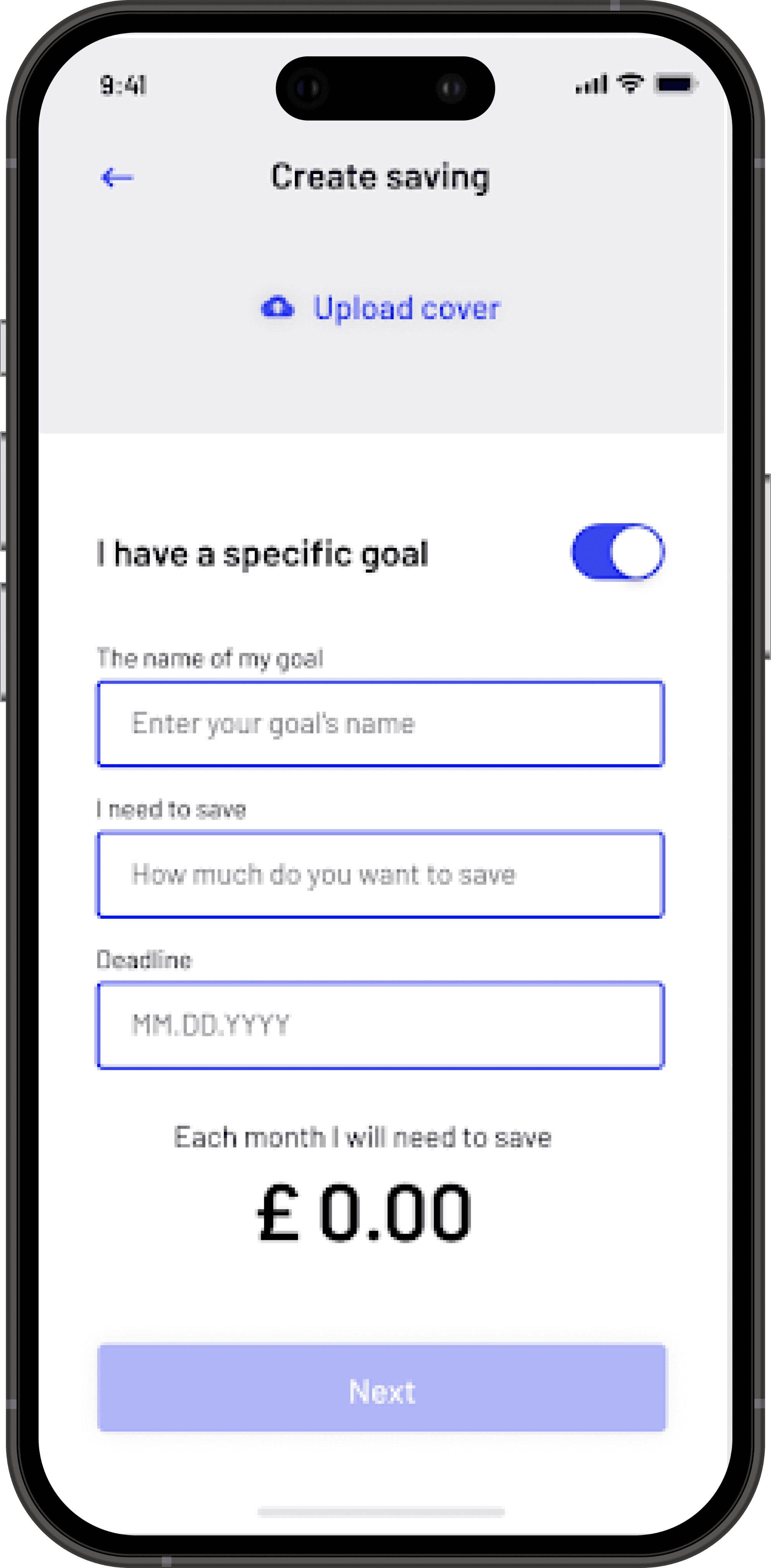

We also learned about the importance of visualizing goals and the extent to which they drive inner motivation and reinforce commitment. So we’ve decided to encourage users to upload a photo of the item or event they are saving for.

There is also the ‘goal gradient effect’, which means that as people get closer to achieving a reward they accelerate their progress toward their goal. People are more motivated by how much is left to reach their target rather than how far they have come.

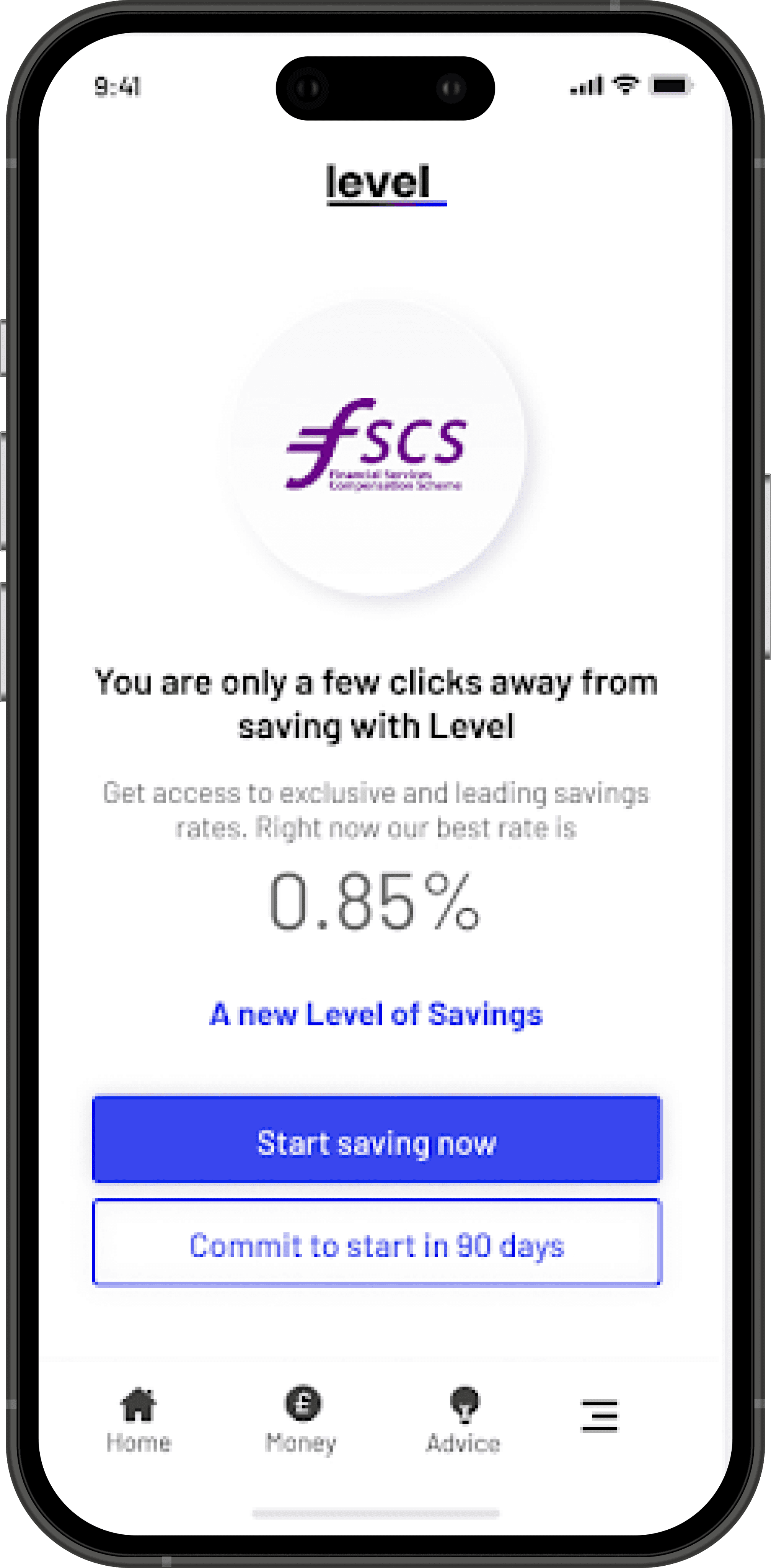

After lots of careful planning and hard work, we launched a super easy savings feature in the app. Now, users can easily set aside some of their earnings for savings. It's all made simple with a smooth interface and visual goal-tracking.

Plus, our app gave out some of the best interest rates around, giving people even more reason to save. We didn't do any official testing, but the whole process was easy to understand, and no issues were reported post-release.

Ideally, if we had the opportunity to track our solution, I would set up at least the following metrics:

User adoption rate of the savings feature

Average savings per user

Percentage of users achieving their savings goals

The integration of the savings feature marked the last significant milestone before the product's official release. With its inclusion in the Level app, users gained access to a powerful tool for financial planning. After rigorous development and testing, the app was successfully launched on both Google Play and the App Store.

The company initiated a strategic partnership with a leading provider of business process services with more than 40 thousand employees, underscoring the app's appeal and potential for widespread adoption within the corporate landscape.

I found that doing some desk research was super helpful in making design choices. It showed me how important it is to use the resources we have, especially when we can't directly talk to users.

This whole experience reminded me how important B2B companies are in looking out for their employees' well-being. It's all about recognizing the big role employers play in shaping people's financial situations.